{{item.videoDuration}}

{{item.title}}

{{item.text}}

{{item.videoDuration}}

{{item.title}}

{{item.text}}

The US economy entered 2023 with more momentum than anticipated, supported by a strong labor market and healthy consumer spending. While encouraging macro data could keep the growth momentum positive near term, higher interest rates, sticky input costs and financial stability risks will weigh on growth in coming quarters.

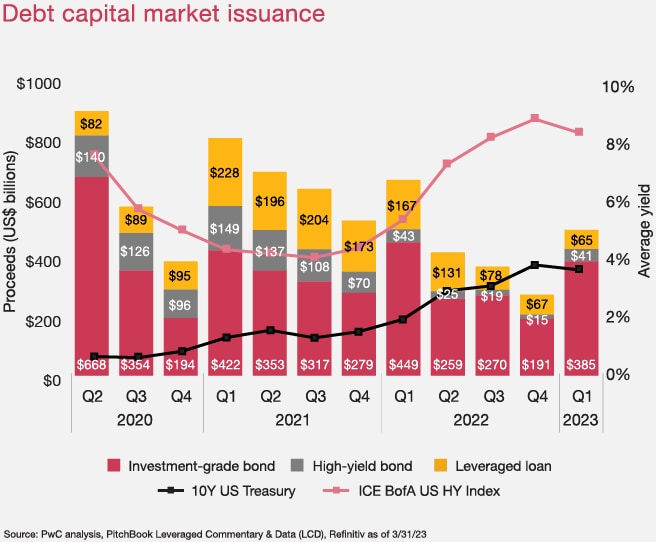

In light of robust employment and shifting inflation data, the Federal Reserve will likely continue to tighten policy. The Fed’s forecast of the terminal rate is 5.1% sometime later in 2023 while PwC is modeling 5.25% to 5.50%. Given recent developments concerning some banks’ liquidity, the Fed will probably continue to focus on broader economic conditions while letting its liquidity facilities address any immediate financial stability concerns.

Increasing risks to financial stability could lead to a tightening in credit conditions and curtail bank lending, leading to lower business investment and consumption growth. The full impact of higher rates on the economy isn’t likely to hit until the second half of this year, pushing back the timing of a potential recession. Even if the US avoids an official recession, economic growth will probably remain below potential.

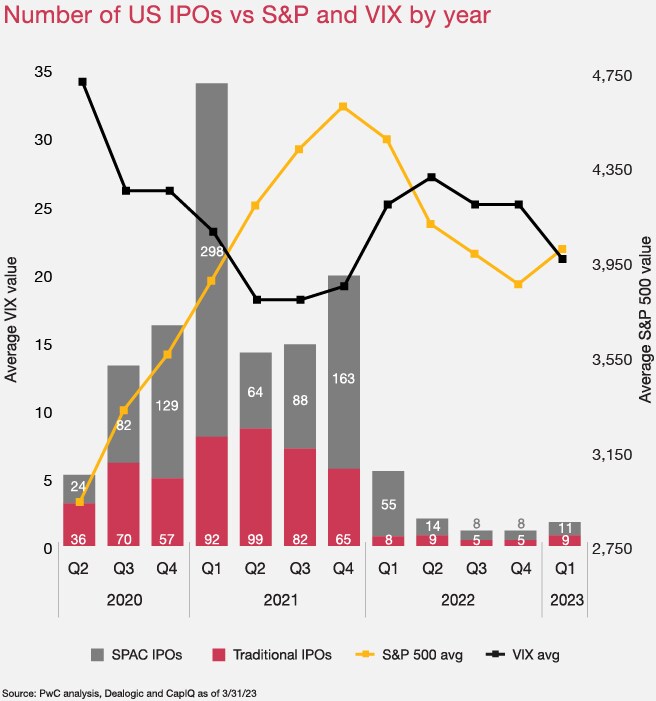

Fewer companies are choosing to go public due to market conditions. Since 2008, the IPO market has mainly been fueled by fast-growing tech and pharma and life sciences companies. Now, most companies planning to list should show a track record of -- or clear path to -- profitability. That’s challenging for many high-growth, high-burn businesses. Several high-profile unicorns that delayed potential IPOs have started searching for new private capital, including debt, to bridge their operations until the market finds surer footing.

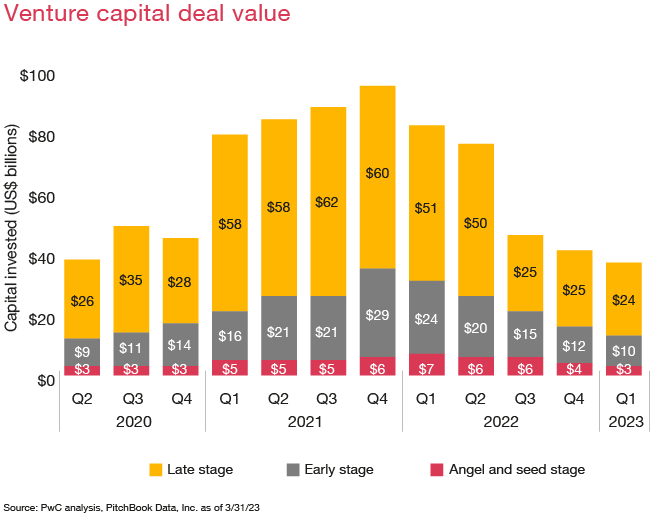

While syndicated M&A and leveraged buyout (LBO) activities have stalled, private equity firms remain active in today’s market. Concerns over profitability, rising costs of debt and a reversion to more conservative underwriting standards have become near-term headwinds. These firms are expected to remain opportunistic amid valuation resets in the public and private markets.

A few factors could help the IPO market improve in late 2023. There’s a backlog of IPO-ready companies needing to raise capital. Confidence in a slight recovery in corporate earnings, continued challenges in the debt market and a gradual waning of market uncertainties also could help.

“While early 2023 showed positive signs for the IPO market with a string of new issuances, recent events have negatively affected market sentiment. There remains significant investable cash on the sidelines that will be more than enough to spark the IPO market into life, as long as a sustained recession is avoided and companies accept the new realities of a reversion to historical valuation levels.”

Note: IPOs with deal values of less than $25 million, best efforts offerings, oil and gas royalty trusts, business development companies, pricing on OTC Bulletin Board and OTC Pink Sheets are excluded from this narrative. Data from SEC filings and third-party databases are as of 3/31/23.

To create a clear path forward, you need the confidence that comes from working with a team of straight-talking advisors and actionable insights from a team of dedicated professionals. Find out how we can guide you through each step of the readiness assessment process and beyond.